312-704-0771

312-704-0771

Recent Blog Posts

How to Collect Money Owed After a Judgment Has Been Issued Against Your Debtor

We have all heard the saying “money is not everything” at some point in our lives. While the phrase is a classic adage for a reason, there are situations in which money is, in fact, the most important thing. It is not uncommon for people to borrow money for a variety of purposes, such as purchasing a home or buying a vehicle. However, when they do not follow their promise to repay that money, they can find themselves in trouble. As a creditor, you have the right to take action against anyone who does not abide by the terms of your repayment agreement. In some cases, this may lead to filing a lawsuit against the debtor. If you are successful, you can then have a judgment entered against your debtor, providing you with several options for collecting the money owed to you.

We have all heard the saying “money is not everything” at some point in our lives. While the phrase is a classic adage for a reason, there are situations in which money is, in fact, the most important thing. It is not uncommon for people to borrow money for a variety of purposes, such as purchasing a home or buying a vehicle. However, when they do not follow their promise to repay that money, they can find themselves in trouble. As a creditor, you have the right to take action against anyone who does not abide by the terms of your repayment agreement. In some cases, this may lead to filing a lawsuit against the debtor. If you are successful, you can then have a judgment entered against your debtor, providing you with several options for collecting the money owed to you.

Citations to Discover

In most cases, the first step taken to recover payment is filing a citation to discover, which is a tool that allows creditors to uncover, freeze, and recover assets from a debtor. A citation to discover creates a continuing lien or freeze on all of the debtor’s eligible property, preventing them from using or disposing of the assets. The main benefit of the citation to discover is that it can uncover all of the assets a debtor has. You will determine which assets you can and cannot focus on recovering to satisfy the amount owed to you.

What Property is Exempt From Illinois Bankruptcy Proceedings?

For many people who are struggling with overwhelming debt, one of the things that holds them back from filing for bankruptcy is the myth that they will lose everything that they own as a result. While it is true that there may be some assets that must be given up during the bankruptcy process, many of these assets are considered exempt property, or property that is not able to be included in the bankruptcy estate. As a creditor, you should know which property is and is not able to be used to repay debts.

For many people who are struggling with overwhelming debt, one of the things that holds them back from filing for bankruptcy is the myth that they will lose everything that they own as a result. While it is true that there may be some assets that must be given up during the bankruptcy process, many of these assets are considered exempt property, or property that is not able to be included in the bankruptcy estate. As a creditor, you should know which property is and is not able to be used to repay debts.

Illinois Property Exemption

When a person files for bankruptcy, they will be assigned a bankruptcy trustee who is responsible for gathering, overseeing, distributing, and/or protecting the debtor’s property that is contained in the bankruptcy estate. The bankruptcy estate contains nearly everything that the debtor owns and is used to pay back creditors in some situations. However, certain property is excluded from being used to repay creditors. This is called exempt property and varies from state to state, in addition to federal exemptions.

When Is it Time to Send a Debt to a Collections Agency?

The COVID-19 pandemic has affected the world in horrific ways. Many people are still experiencing financial difficulties because of the pandemic. Various types of businesses across the country were shut down for months at the height of the pandemic, leaving millions of people without a job and without income. Now, a year later, the economy is slowly starting to pick back up, but many people are still struggling financially and missing payments on debts they owe. As a lender, not receiving payments can also be financially burdensome, forcing you to take action. In many cases, a lender will send an individual’s debt to a collection agency. However, sending a debt to collections is a big decision to make that could greatly affect the borrower and have an impact on the amount you receive. How do you know if sending a debt to collections is the right call?

The COVID-19 pandemic has affected the world in horrific ways. Many people are still experiencing financial difficulties because of the pandemic. Various types of businesses across the country were shut down for months at the height of the pandemic, leaving millions of people without a job and without income. Now, a year later, the economy is slowly starting to pick back up, but many people are still struggling financially and missing payments on debts they owe. As a lender, not receiving payments can also be financially burdensome, forcing you to take action. In many cases, a lender will send an individual’s debt to a collection agency. However, sending a debt to collections is a big decision to make that could greatly affect the borrower and have an impact on the amount you receive. How do you know if sending a debt to collections is the right call?

Reasons to Consider Debt Collection

3 Ways Banks Can Stay Proactive to Prevent Debtor Delinquency

This past year has been difficult for many people because of the ongoing COVID-19 crisis. Across the country, people and businesses alike have had trouble making ends meet, with many comparing this situation to the Great Recession in the late 2000s. According to the American Bankers Association (ABA), consumer credit delinquencies rose at the end of 2020, despite those numbers decreasing in the prior two quarters. All 11 loan categories saw an increase in the number of delinquent accounts, with home equity and mobile home loans seeing the largest increase. Nobody likes a late-paying customer, but there are ways banks can help keep the number of your delinquent accounts to a minimum.

This past year has been difficult for many people because of the ongoing COVID-19 crisis. Across the country, people and businesses alike have had trouble making ends meet, with many comparing this situation to the Great Recession in the late 2000s. According to the American Bankers Association (ABA), consumer credit delinquencies rose at the end of 2020, despite those numbers decreasing in the prior two quarters. All 11 loan categories saw an increase in the number of delinquent accounts, with home equity and mobile home loans seeing the largest increase. Nobody likes a late-paying customer, but there are ways banks can help keep the number of your delinquent accounts to a minimum.

Be Proactive With Your Customers

The best way to deal with delinquent customers is to try to prevent them from becoming past-due. You can do this by implementing a number of practices, like email communications, notices through the mail, or phone calls. Giving your customers multiple reminders about upcoming payments may help prevent their accounts from going delinquent.

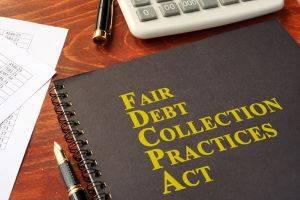

Understanding the Laws Governing Actions Taken by Debt Collection Agencies

Those who always pay off their credit card balances at the end of every month and pay all of their other debts on time may never come into contact with a debt collection agency. A debt collection agency is a separate company that many lenders and creditors use to facilitate the retrieval of unpaid debts from consumers. Most of the time, hiring a debt collection agency is used as a last resort, after a creditor has already tried and failed several times to recover the payments themselves. A debt collector can be a good choice for some lenders and finance companies, but there are federal rules and regulations that they are subject to. Before hiring a debt collection agency, you should be aware of the limitations they have.

Those who always pay off their credit card balances at the end of every month and pay all of their other debts on time may never come into contact with a debt collection agency. A debt collection agency is a separate company that many lenders and creditors use to facilitate the retrieval of unpaid debts from consumers. Most of the time, hiring a debt collection agency is used as a last resort, after a creditor has already tried and failed several times to recover the payments themselves. A debt collector can be a good choice for some lenders and finance companies, but there are federal rules and regulations that they are subject to. Before hiring a debt collection agency, you should be aware of the limitations they have.

Rules for Debt Collection Agencies

Debt collection agencies will typically try various methods to retrieve past-due debt, including calling the debtor, mailing delinquent notices to the debtor’s address, and even visiting the debtor’s residence in extreme circumstances. The Federal Trade Commission (FTC) is the governing body that oversees the practices of debt collection agencies to ensure everyone is in compliance with the Fair Debt Collection Practices Act (FDCPA). According to the FDCPA, forbidden actions by debt collection agencies include:

Can a Creditor Lift the Automatic Stay During a Bankruptcy Case?

For many people, one of the fairly attractive parts of filing for bankruptcy is the automatic stay that takes place when they file a bankruptcy petition. This automatic stay will require creditors to cease all collection activity while the bankruptcy case is ongoing. This means that you, as a creditor, can no longer contact the debtor in any way or have another agency or individual contact them on your behalf for purposes of collecting debt. The discharge of debt through bankruptcy typically results in some sort of financial loss, which can put stress on any business. If your debtor has filed for bankruptcy, there are certain cases in which you can file for a motion to lift the automatic stay with the bankruptcy court, which would allow you to continue collection practices.

For many people, one of the fairly attractive parts of filing for bankruptcy is the automatic stay that takes place when they file a bankruptcy petition. This automatic stay will require creditors to cease all collection activity while the bankruptcy case is ongoing. This means that you, as a creditor, can no longer contact the debtor in any way or have another agency or individual contact them on your behalf for purposes of collecting debt. The discharge of debt through bankruptcy typically results in some sort of financial loss, which can put stress on any business. If your debtor has filed for bankruptcy, there are certain cases in which you can file for a motion to lift the automatic stay with the bankruptcy court, which would allow you to continue collection practices.

What You Should Include in Your Motion

How Can a Judgment Enforcement Attorney Help You?

Whether you are from a bank, a credit union, an auto lender, an equipment lender, a truck lender, or another financial institution that might be involved in bankruptcies or other debt collection activities, you might find that sometimes you need more assistance with judgment enforcement. Simply having a judge declare that money or other assets are owed to you or whoever you represent might not be enough to repossess or recover the assets from the debtor. For instance, the debtor might be ignoring your phone calls and letters or the debtor might be hiding the assets you are trying to repossess. Whatever the case may be, using the full power of the law at your disposal is a good idea to recover what the courts determine is yours. That is when you should call upon a professional judgment enforcement attorney to learn what they can do for you.

How Will Cryptocurrency Affect Debt Collection in the Future?

As someone from a credit union, bank, or other financial institution, among other organizations, who deal with debt collection activities every day, sooner or later, you will have to deal with Bitcoin and other cryptocurrencies, if you have not already and whether you want to or not. This is because, over the last several years, cryptocurrency has made tremendous strides in the following ways:

-

Multibillion-dollar investors from leading companies have been investing in cryptocurrencies like Bitcoin to get ahead of the trend, increasing its value and popularity amongst investors.

-

Cryptocurrency infrastructure is finally safe and easy relative to its possible “dark web” roots and other suspicions of illegitimacy.

What You Need to Know About the President’s Plans for Credit Reporting

You might not be aware of it, but one of President Biden’s campaign promises was to make credit reporting fairer and more accurate so that everyone across the country, no matter their race or socioeconomic status, can have more equal and much better opportunities to access credit cards, loans, mortgages, and other financial offerings. As a representative from an auto lender, equipment lender, truck lender, credit union, bank, or other financial institution, you might want to learn more about the possibilities that the Biden Administration is open to with regards to credit reporting reform. Here are some new ideas that you might see over the next four years. Keep them in mind during your dealings with debt collection activities, including bankruptcies.

How Can a Forensic Accountant Help With Your Debt Collection Duties?

As a financial professional, be it as a representative from a credit union, bank, auto lender, truck lender, equipment lender, or other financial institution, it is important to work with an attorney who acts as an official litigator. Together, you might think you have everything taken care of when it comes time to investigate the finances of a debtor you suspect might be committing fraud or other wrongdoing. However, with regards to any number of debt collection activities, including such complicated legal processes as bankruptcy, you could also benefit from the assistance of a forensic accountant.

Contact Our Firm

The use of the Internet or this form for communication with the firm or any individual member of the firm does not establish an attorney-client relationship. Confidential or time-sensitive information should not be sent through this form.

The use of the Internet or this form for communication with the firm or any individual member of the firm does not establish an attorney-client relationship. Confidential or time-sensitive information should not be sent through this form.

I have read and understand the Disclaimer and Privacy Policy.